All Categories

Featured

2 individuals purchase joint annuities, which supply a surefire earnings stream for the remainder of their lives. When an annuitant passes away, the passion made on the annuity is handled in different ways depending on the kind of annuity. A type of annuity that stops all repayments upon the annuitant's death is a life-only annuity.

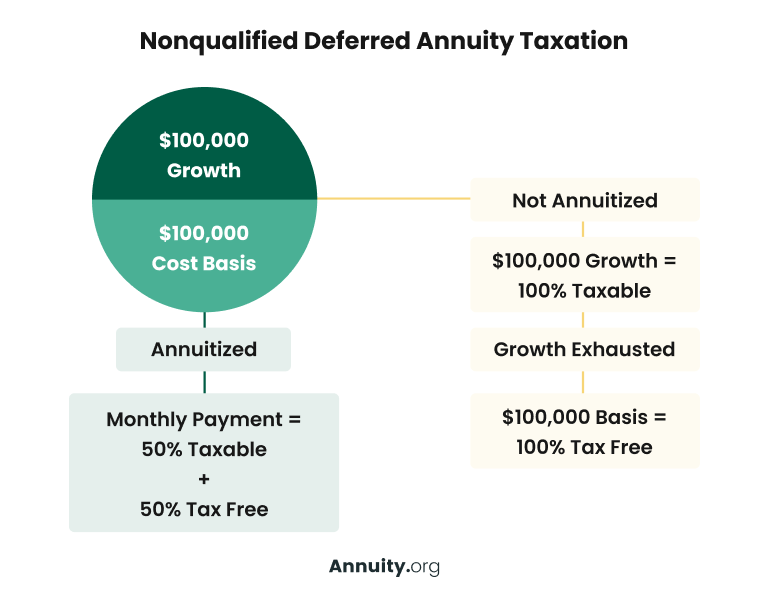

The original principal(the amount originally deposited by the moms and dads )has actually currently been tired, so it's not subject to tax obligations again upon inheritance. Nonetheless, the earnings portion of the annuity the interest or investment gains built up in time is subject to income tax obligation. Normally, non-qualified annuities do.

have died, the annuity's advantages usually return to the annuity owner's estate. An annuity owner is not legitimately needed to notify current recipients about modifications to recipient designations. The decision to alter recipients is generally at the annuity proprietor's discernment and can be made without notifying the existing beneficiaries. Given that an estate practically does not exist until an individual has actually died, this recipient classification would just enter effect upon the fatality of the named person. Typically, as soon as an annuity's proprietor passes away, the assigned recipient at the time of death is entitled to the advantages. The partner can not transform the beneficiary after the owner's death, also if the recipient is a small. There might be particular provisions for handling the funds for a small recipient. This commonly involves selecting a guardian or trustee to take care of the funds up until the child gets to adulthood. Generally, no, as the beneficiaries are not responsible for your debts. It is best to get in touch with a tax obligation specialist for a certain solution relevant to your situation. You will certainly proceed to obtain repayments according to the contract routine, but attempting to get a swelling sum or loan is most likely not a choice. Yes, in mostly all cases, annuities can be inherited. The exception is if an annuity is structured with a life-only payment option via annuitization. This sort of payout stops upon the death of the annuitant and does not offer any recurring value to beneficiaries. Yes, life insurance policy annuities are normally taxable

When taken out, the annuity's revenues are exhausted as regular earnings. The principal amount (the initial investment)is not tired. If a recipient is not named for annuity benefits, the annuity continues generally go to the annuitant's estate. The circulation will follow the probate process, which can postpone repayments and might have tax obligation ramifications. Yes, you can call a trust fund as the recipient of an annuity.

Taxes on inherited Annuity Payouts payouts

This can offer greater control over just how the annuity advantages are distributed and can be part of an estate planning approach to take care of and secure properties. Shawn Plummer, CRPC Retired Life Coordinator and Insurance Agent Shawn Plummer is a certified Retirement Coordinator (CRPC), insurance coverage agent, and annuity broker with over 15 years of direct experience in annuities and insurance. Shawn is the owner of The Annuity Professional, an independent online insurance policy

company servicing customers across the United States. With this platform, he and his team aim to get rid of the uncertainty in retirement planning by helping people discover the very best insurance protection at one of the most affordable prices. Scroll to Top. I understand all of that. What I don't recognize is exactly how previously getting in the 1099-R I was showing a reimbursement. After entering it, I currently owe tax obligations. It's a$10,070 distinction between the refund I was anticipating and the taxes I now owe. That appears really extreme. At many, I would have expected the refund to decrease- not completely go away. An economic advisor can assist you make a decision how finest to take care of an inherited annuity. What happens to an annuity after the annuity owner dies depends upon the regards to the annuity agreement. Some annuities merely quit distributing income repayments when the owner dies. In most cases, nevertheless, the annuity has a survivor benefit. The recipient could obtain all the remaining money in the annuity or an assured minimum payout, generally whichever is higher. If your parent had an annuity, their contract will define that the recipient is and might

right into a pension. An inherited individual retirement account is an unique pension utilized to disperse the assets of a dead individual to their beneficiaries. The account is signed up in the deceased individual's name, and as a beneficiary, you are unable to make extra payments or roll the acquired individual retirement account over to an additional account. Just certified annuities can be rolledover into an inherited individual retirement account.

{kind=link}

Latest Posts

Understanding Fixed Annuity Or Variable Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Annuity Or Variable Annuity Benefits of Variable Annuity Vs Fixed Annuity

Highlighting Variable Annuity Vs Fixed Annuity Key Insights on What Is Variable Annuity Vs Fixed Annuity What Is the Best Retirement Option? Benefits of Choosing the Right Financial Plan Why Choosing

Analyzing Annuity Fixed Vs Variable A Closer Look at Fixed Income Annuity Vs Variable Growth Annuity Defining Retirement Income Fixed Vs Variable Annuity Benefits of What Is A Variable Annuity Vs A Fi

More

Latest Posts